The Massachusetts Health Policy Commission presented this slide deck at the annual Cost Trends Hearings. It is a good descriptor of some key performance indicators of the state's health care system. Here's the key summary page (as I read the report):

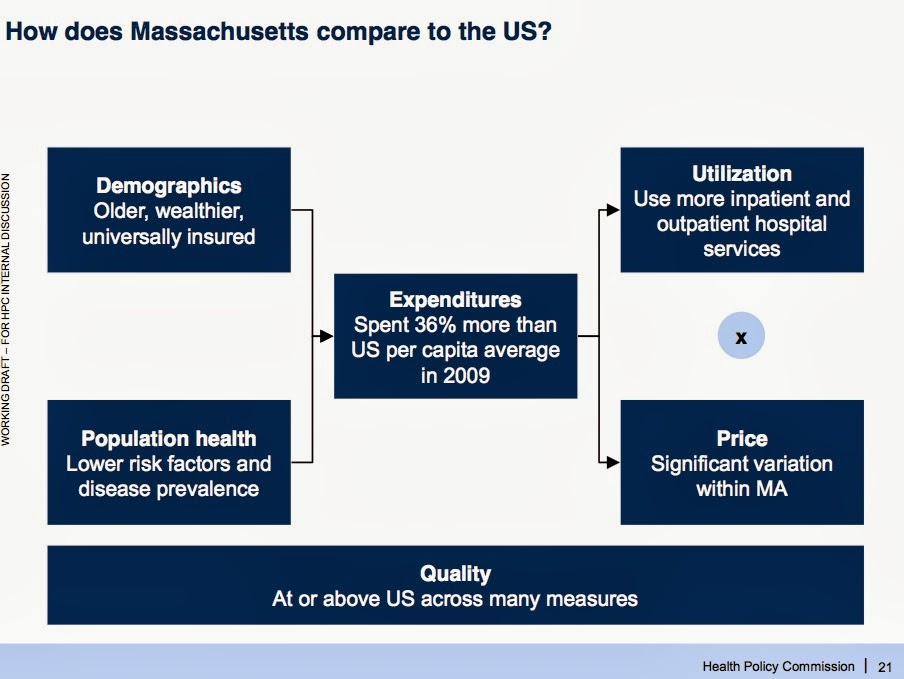

In case you can't read it, the summary is that the state spent 36% more than the US per capita average in 2009; that the demographic indicators show an older, wealthier, universally insured population that has lower risk factors and disease prevalence than the average. The population uses inpatient and outpatient services more than the national average. On the price front, there is significant variation within the state. Finally, there is an assertion that quality is at or above the US for many measures.

Recent growth in per capita expenses are less than the national average. For 2009-2012, MA expenses grew at 1.9% compared to a national figure of 3.1%. For 2000-2009, MA grew at a higher rate than the national average, 6.8% versus 5.7%.

The report does not reach conclusions about the cause for the slowdown. It asks the following questions:

How can we maintain the progress of the last few years?

Where can we go further on utilization and price?

Where are opportunities for plans, providers, employers, consumers, and the state to play a role?

That no answers are given to the questions raised is not unexpected. I doubt whether there would be a consensus even within the HPC as to the answers, much less across the public. Those advocating a wide range of public policy and private directions for the future can all find support for their positions in this document.

In short, the report provides a good touchstone and reference report for the future.

In case you can't read it, the summary is that the state spent 36% more than the US per capita average in 2009; that the demographic indicators show an older, wealthier, universally insured population that has lower risk factors and disease prevalence than the average. The population uses inpatient and outpatient services more than the national average. On the price front, there is significant variation within the state. Finally, there is an assertion that quality is at or above the US for many measures.

Recent growth in per capita expenses are less than the national average. For 2009-2012, MA expenses grew at 1.9% compared to a national figure of 3.1%. For 2000-2009, MA grew at a higher rate than the national average, 6.8% versus 5.7%.

The report does not reach conclusions about the cause for the slowdown. It asks the following questions:

How can we maintain the progress of the last few years?

Where can we go further on utilization and price?

Where are opportunities for plans, providers, employers, consumers, and the state to play a role?

That no answers are given to the questions raised is not unexpected. I doubt whether there would be a consensus even within the HPC as to the answers, much less across the public. Those advocating a wide range of public policy and private directions for the future can all find support for their positions in this document.

In short, the report provides a good touchstone and reference report for the future.

0 comments:

Post a Comment